Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

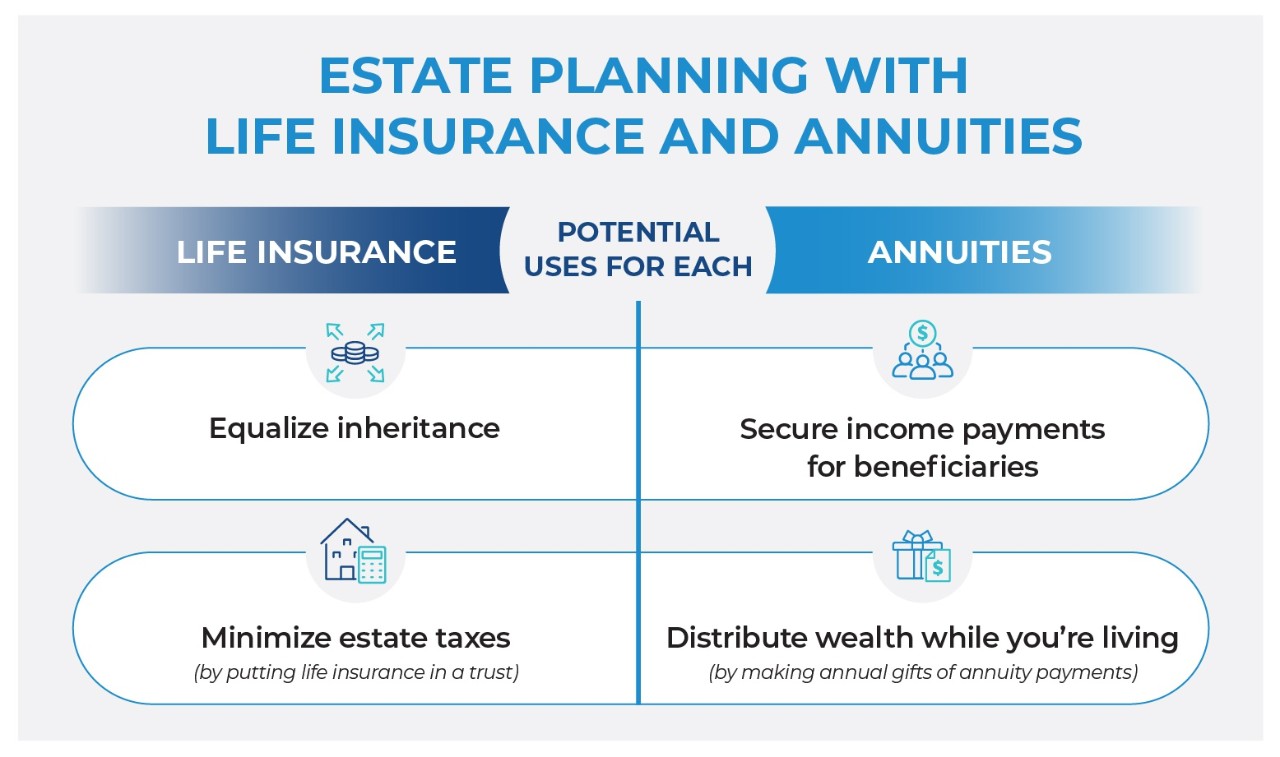

Adding these two financial products could help you achieve your estate planning goals more efficiently.

How does life insurance fit into estate planning?

The primary goal of life insurance is to provide a death benefit for family or other beneficiaries to help pay for immediate financial needs or replace lost income. But adding life insurance to an estate plan can go beyond a simple death benefit by helping you to equalize an estate or minimize the potential estate tax bite. And, if you plan to leave behind a large estate, a life insurance death benefit can also be used to help maximize estate planning legacy goals by helping beneficiaries pay estate taxes that might be due.

Equalizing an inheritance

Owners of estates that contain real estate, artwork, or other hard-to-liquidate assets may want to include life insurance in their estate plans to help even out the inheritance between siblings or other beneficiaries. For example, if you own real estate but only one of your children lives nearby or is interested in inheriting that property, you can use life insurance proceeds to help equalize the inheritance for your other children, instead of having to divide and sell property that you’d like to remain in the family.

Estate planning with a life insurance trust

If your estate is larger than that allowed by estate tax exemption limits, you may want to consider establishing an irrevocable life insurance trust and using some of your assets to fund the purchase of a life insurance policy. When a life insurance policy is owned by a properly structured irrevocable trust, the death benefit passes to the beneficiaries outside of your estate, which may provide greater tax efficiency. That also means that the policy is no longer your asset and potentially not under your control. However, you can work with your financial professional to set up the trust in the way you want — for example to benefit your spouse, a charity, or a child with special needs, which are just a few potential options. There are many types of trusts for different purposes, so talk to your financial professional, tax or legal advisor to learn more.

How does an annuity fit into estate planning?

An annuity is a financial product that can offer protected lifetime income and even potentially grow your money. Many people think of annuities as retirement savings and income vehicles. However, they can also be a beneficial addition to estate plans.

- Give beneficiaries a stream of income, not a lump sum. If your heirs need the money you’ll leave them but may not be great at budgeting or might be inclined to overspend a lump sum, part of your estate plans may include setting up an annuity that can give your beneficiaries the stability and security of guaranteed income payments instead. If you purchase a deferred annuity (one that provides income at some later date), that money has the potential to grow tax-deferred, creating additional income as well.

- Make annual gifts to heirs while you’re living. If you don’t need the money from an annuity for your own retirement or living expenses, you can make an annual gift of annuity income payments to your loved ones while you’re alive and able to see the benefits of that money firsthand. In this case, estate planning can mean distributing money from your estate before you pass away.

Regardless of your estate planning goals, you may find the flexibility, security and control of life insurance and annuities to be beneficial. Talk to your financial professional about the options available to you and whether they might be a good fit for you.

READ MORE

In order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life refers to Pacific Life Insurance Company and its subsidiary Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company and in all states by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

PL76