Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

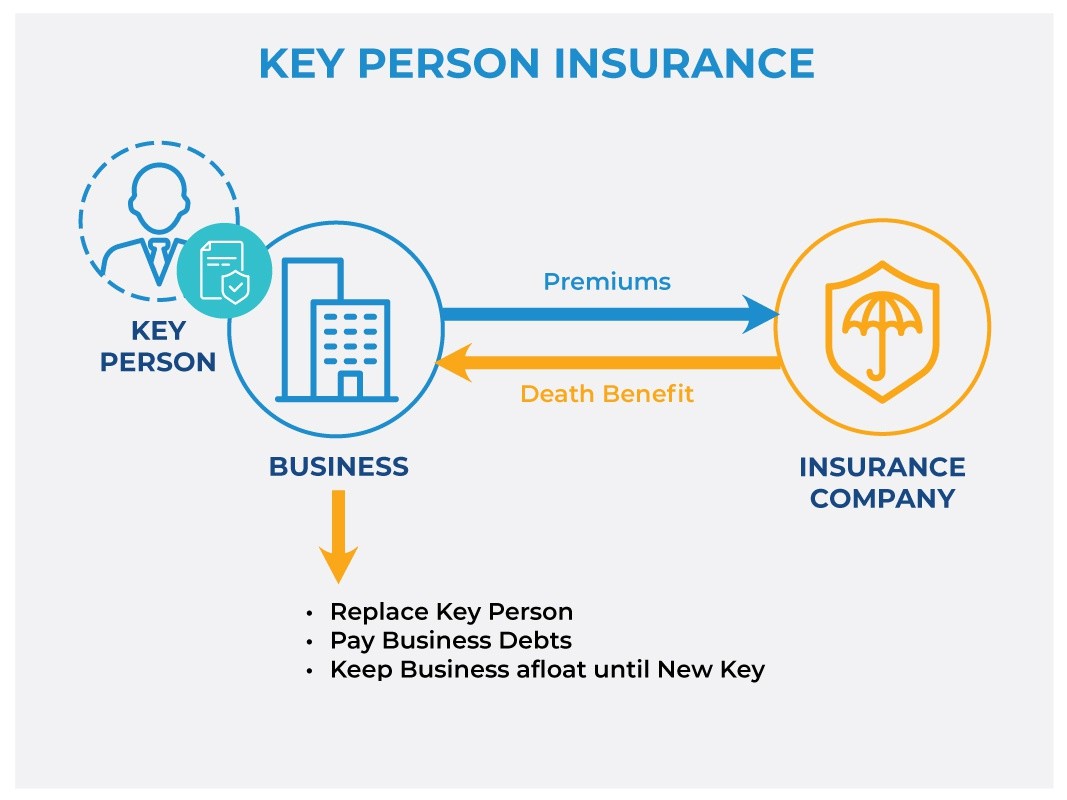

Life insurance for an employee your business can’t live without

Small businesses often have at least one employee with a unique skillset, stellar reputation, loyal client base, or an all-star name, whose absence would devastate the company. If you have an owner, partner, executive, or other worker who is indispensable, you may want to consider key person life insurance to protect your business from the potential loss of this essential employee.

What is key person life insurance?

Key person life insurance is a type of life insurance that is purchased by a business on an essential employee, with the employee’s written consent. The business pays the premiums and then receives the death benefit if the key employee dies unexpectedly.

When might you need key person life insurance?

There are a number of reasons you might want to protect your business from the loss of a key employee by purchasing a key person life insurance policy.

- Reputation. If your company’s reputation is linked to that of a key person’s name, reputation, or unique skills, their loss might mean a significant drop in business. The policy’s death benefit can help you shore up your company and give you time to find a suitable replacement.

- Loans. If your business is seeking investors or taking loans, the lenders might be hesitant to provide that money without a life insurance policy in place on key personnel.

- Financial burden. If the loss of your key employee would cause an undue financial burden on the company — because they’re in a highly specialized role that would be difficult to replace, or they bring in a large percentage of the company’s revenue — having some extra cash available to tide you over if something happens to them might be vital to keeping your business afloat.

- Partners. If there is more than one owner and everyone agrees that they’d like to keep the business, having key person insurance on each owner can provide the cash to buy out the deceased’s estate and continue the business with the surviving owners. This is typically done as part of a buy-sell agreement.

- Sole owner. If you’re the sole owner of the business and you plan to close the business when you pass away, life insurance will give your beneficiaries the cash to pay off your debts and shutter the company.

How much life insurance is necessary on a key person?

If you are purchasing key person life insurance to cover a loan or investment, the amount you need is simple: enough to repay the loan or cover the investment. If you’re using life insurance to protect your company for other reasons, you may want to consider the impact that employee’s loss would have on the business. What percentage does this person contribute to your company’s bottom line? What is their current salary? How much might you lose in sales? How long will it take you and how much will it cost to replace this person? Will there be a loss in productivity across the company or in key areas? As a general rule of thumb, the amount of key person coverage should be 5 to 10 times the key employee's annual salary.

Consider the type of key person life insurance policy for your needs

You can choose between a term policy or a cash-value policy. A term key person life insurance policy will pay a cash benefit if the key person dies within the specified time period (typically 10, 15, or 20 years), and may be a good option if you only need protection during that time. A cash-value key person life insurance policy, on the other hand, will cover the key person for life or as long as you stay current on the premiums. Cash-value policies often cost more, but can also provide the potential for a buildup of cash value, which you may be able to access from the policy via loans or withdrawals to cover other expenses.

Talk to your financial professional about your situation and if a key person life insurance policy may be a good idea for your company.

READ MORE

In order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life refers to Pacific Life Insurance Company and its subsidiary Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company and in all states by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

PL80