Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

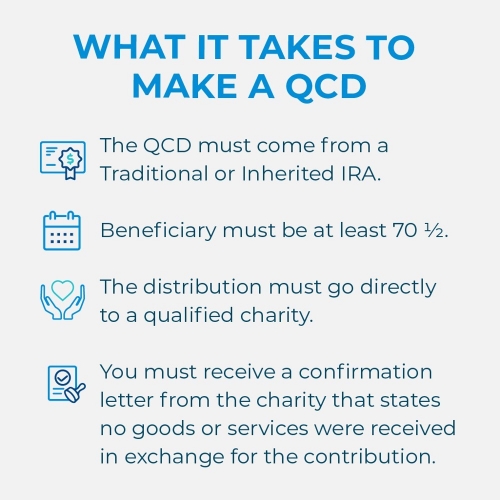

Qualified charitable distributions can help with tax savings and at the same time give to charity during retirement.

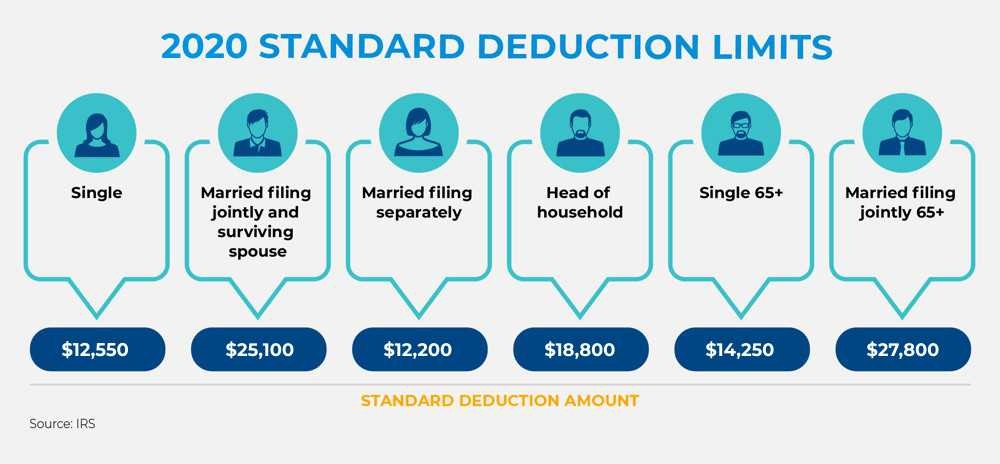

You may have noticed that the Tax Cuts and Jobs Act of late 2017 has had an effect on how you give to charities. The act doubled the standard deduction, which is now $12,550 for individuals and $25,100 for married couples filing jointly in 2020. If you’re over 65, there’s an additional deduction of $1,350 per spouse for married couples filing jointly and $1,700 if you’re single. As a result, unless your itemized deductions are above this relatively high threshold, you don’t receive extra tax benefits for charitable giving.

However, if you’re retired and receiving required minimum distributions (RMDs), qualified charitable distributions (QCDs) are an alternative way to give that can help you lower your taxes and achieve other savings.

What is a QCD?

The Pension Protection Act of 2006 created QCDs, and Congress made them permanent in 2015. Under the law, if you’re at least 70½ you can give up to $100,000 each year directly from your IRA to a qualified public charity.

An RMD is the government-mandated amount that you must withdraw each year from your retirement plans. Typically, when you take an RMD the money is counted toward your modified adjusted gross income (MAGI). As a result, the RMD increases your taxable income.

However, if you donate the RMD directly to a qualified charity using a QCD instead, the RMD bypasses your income. It will not affect your MAGI. As a result, you may have a lower income tax bill than if you’d received all the RMDs yourself. Your CPA or financial professional can help you make a QCD and maximize its benefits.

When QCDs are most efficient

QCDs work best if you don’t tend to itemize your deductions. That’s because once you make a QCD, you cannot count it as a deduction and the QCD will not help bump you over the threshold of the standard deduction. Now that the standard deduction is relatively high, you may find yourself among those who don’t itemize. QCDs may also be useful for those whose RMDs would otherwise push them into a higher tax bracket, triggering higher income or capital gains taxes.

If you do itemize, there may be more tax efficient ways of giving than with a QCD. For instance, you may prefer to donate highly appreciated securities that could trigger a high capital gains tax bill were you to you sell them.

Other ways QCDs can help

Beyond potential tax savings, QCDs can help lower Medicare premiums. Here’s how it works: Your MAGI determines whether an income-related monthly adjustment amount applies to your Medicare Part B premiums, which are determined by annual income. Couples filing jointly with a MAGI of $176,000 or less can expect to pay $148.50. Couples with an MAGI of $176,000 to $222,000 can expect to pay $207.90. When you lower your MAGI, you may in turn lower your premiums.

The size of your MAGI also has an effect on the taxability of your Social Security benefits, your eligibility to contribute to a Roth IRA and how much Medicare tax you pay. If you’re looking to manage these factors and your tax bill, the QCD remains a powerful strategy to help you give to the charities of your choice.

READ MORE

The above is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with their accounting or tax professionals for guidance regarding your specific financial situation.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL44A