Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

A plan that includes life insurance can help provide liquidity and equality in a family business succession.

If you’ve spent a lifetime building a family business, you may find that it’s among your most important assets. A carefully developed succession plan can help you engineer a smooth transition into the company’s next phase, whether you plan to sell the business or pass it on to your heirs after you’re gone. The type of life insurance policy you choose can play a key role in that plan. Though the primary role of life insurance is to protect against premature death, it can also be used as a tool to help you divide your estate or provide liquidity to keep your business running after you’re gone.

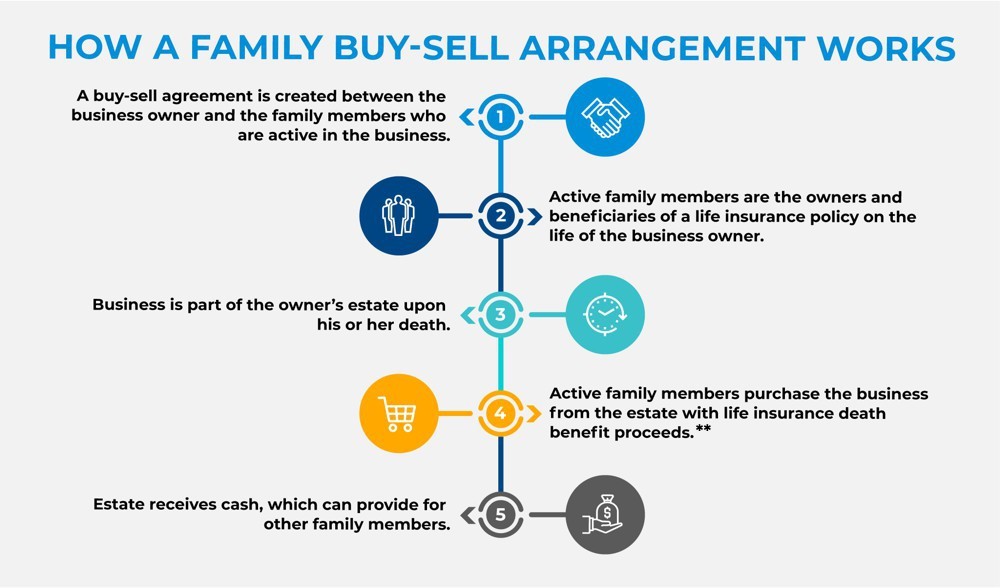

If you have family members active in the business that you would like to take over when you are gone, a family buy-sell arrangement involving life insurance may be appropriate.

Equality among heirs

Deciding how to divide a family business among heirs can be fraught with challenges. In some cases, each heir may be involved in the business, and the shares can be divided equally. If one or more of your heirs doesn’t want to help run the company, however, including a life insurance policy in your succession plan can help divide your estate fairly.

Say you have three children, two of whom are active in the family business and a third who is not. You want to leave an equal inheritance to all three, but simply dividing the business evenly among them could lead to potential challenges and conflict between the siblings who are active in the business and the sibling who is not.

Life insurance, along with other tools, can provide a way to address this conundrum.

Liquidity for a smooth transition

A family buy-sell arrangement provides a way to pass along a family business to your family members who are active in the business while also providing for a surviving spouse or other heirs who are not active in the business. Under this type of arrangement, there would be a buy-sell agreement between you and your family members who wish to remain active in the business. To fund the buy-sell, the active family members could be the owners and beneficiaries of a life insurance policy on your life.

When you die, your business is included in your estate,* and the death benefit proceeds from the life insurance policy go to the active family members income tax-free.** They can then use these funds to purchase the business from your estate under the terms of the buy-sell agreement. In this way, your business passes only to family members who are active in it, and cash is made available as a result of the purchase of the business from your estate to provide for family members who don’t want to participate in the business.

Also consider a key person life insurance policy to help cover the financial impact of the loss of a key employee. This type of policy, of which the business is the owner and beneficiary, can be especially valuable for businesses that depend heavily on a small number of individuals whose skills or expertise would be difficult to replace. Key person insurance can cover the lost revenue and/or profits the business would experience as result of the loss of the key employee, as well as the cost of recruiting and training a replacement.***

Determining the fate of a family business can be a challenging emotional process. By planning ahead, you may avoid potential conflict and set up your business—and your family—to thrive for generations to come.

READ MORE

* According to the Tax Cuts and Jobs Act of 2017, the federal estate, gift and generation-skipping transfer (GST) tax exemption amounts are all $10,000,000 per person (indexed for inflation effective for tax years after 2011); the maximum estate, gift and GST tax rates are 40%. In 2026, the federal estate, gift and GST tax exemption amounts are scheduled to revert to $5,000,000 per person (indexed for inflation for tax years after 2011).

** For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2) (i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

*** In order to preserve the tax-free death benefit the business must get written notice and consent before the policy is issued under 101(j).

The above is provided for informational purposes only and should not be construed as investment, tax or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with your accounting or tax professional for guidance regarding your specific financial situation.

The results and explanations generated by the tool on this page may vary due to user input and assumptions. Pacific Life does not guarantee the accuracy of the calculations, results, explanations, nor applicability to your specific situation. We recommend that you use this calculator as a guideline only and ultimately seek the guidance of an experienced professional. CalcXML, the provider of this information and interactive calculator, is an independent third-party and is not affiliated with Pacific Life.

This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL42A