Doing all you can to protect your loved ones

You want the best for your family. But have you explored all your options for sheltering them from life's storms?

View our infographic for interesting fact & figures about life insurance.

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

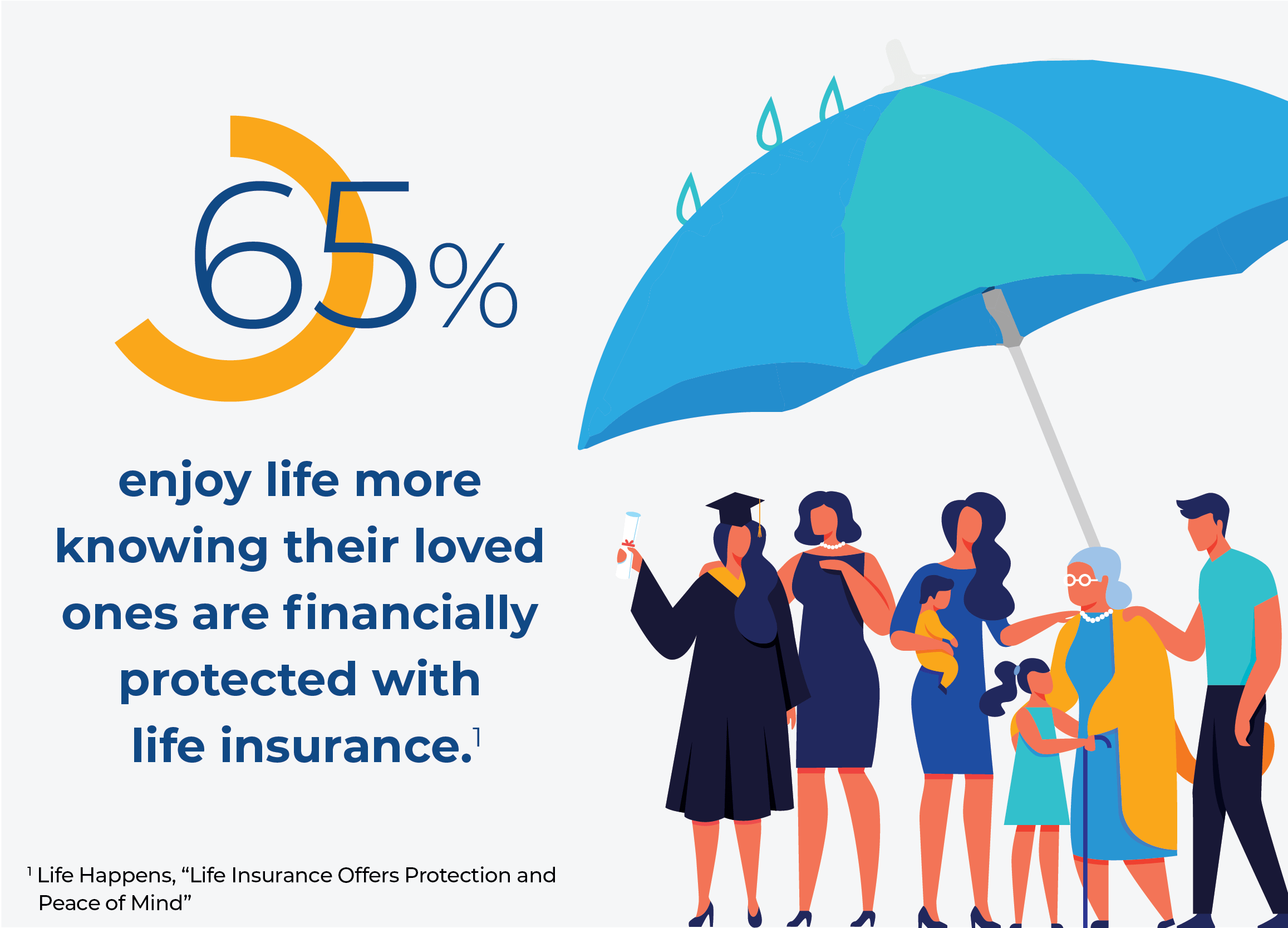

You take care of your family every day, from providing for your kids to nurturing your spouse. You do it because you love them—and because you’re responsible for them. While you may not always be here, with a bit of planning you can leave a financial safety net and legacy for your loved ones.

Simple steps can make a big difference, like naming and updating beneficiaries on existing retirement accounts and life insurance policies; engaging in basic estate planning, such as writing a will so everyone knows your wishes; and buying adequate life insurance. All these moves can help your family thrive when you’re no longer with them. Talk to a financial professional about how you can protect your family today and in years to come.

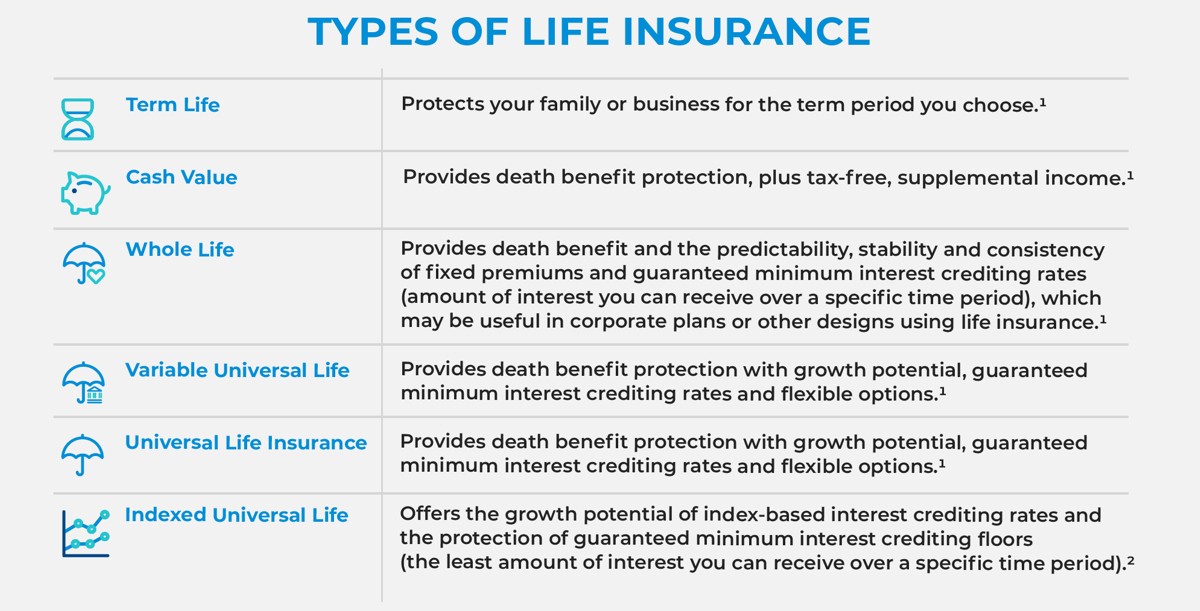

Life insurance provides security for all kinds of families, from those with younger children, to empty nesters and older couples without children who use cash value policies as part of an overall retirement income strategy. A financial professional can help you decide which type of life insurance works best for you. For instance, term policies, good for a set number of years, are often less costly, and they’re popular with young families because they help survivors resolve debt and maintain their lifestyle. Cash value life insurance policies have a cash value accumulation component that allows the flexibility of using the money earned while you’re still here to enjoy it.

Sources:

1 The American Council of Life Insurers, “Types of Life Insurance”

2 Pacific Life, Glossary

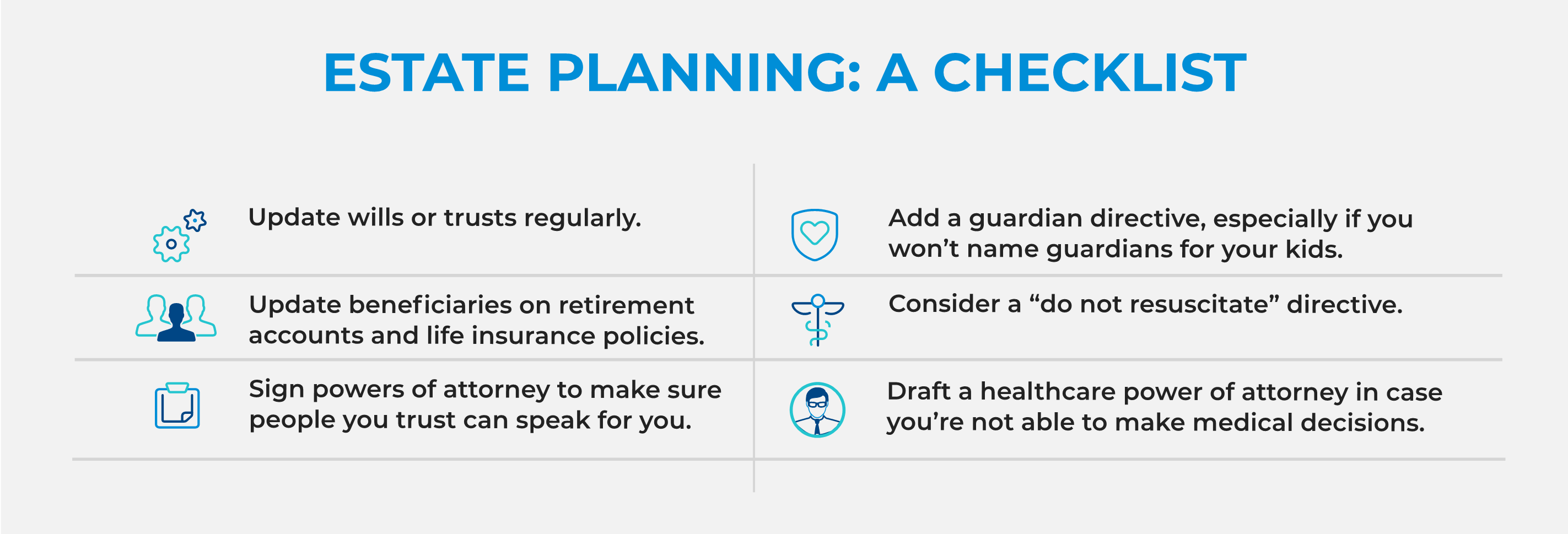

Estate planning is crucial for anyone—regardless of income or assets—who cares about having their wishes carried out the way they want. From who will care for your children to how much you leave to charity, the only way to communicate those desires once you’re gone is by having the right documents in place. A financial professional can help you create an estate plan that best suits the needs of your family.

There’s no one-size-fits-all answer to this question. Everyone has different financial situations and goals, and every family has different needs. Your goal may be to help replace lost income, including lost 401(k) contributions, or to ensure each child has college tuition, plus help your spouse pay off the mortgage. Cash value life insurance policies offer growth potential that can supplement retirement income streams. Life insurance may also help secure your financial legacy for heirs or even favorite charities. With help from a financial professional, you can land on the right amount of life insurance to meet your goals. Our Life Insurance Calculator can help you start the analysis.

You want the best for your family. But have you explored all your options for sheltering them from life's storms?

View our infographic for interesting fact & figures about life insurance.

Death benefit protection with tax deferred cash value build up, and ability to access the cash value via policy loans and withdrawals.

A fixed indexed annuity is designed to provide reliable monthly income that lasts for life. It protects your principal, while providing growth opportunity based on the positive movement of an index, such as the S&P 500® index. Fixed indexed annuities enable you to grow your retirement savings faster by deferring taxes until you take income, creating lifetime income, and providing for loved ones through a guaranteed death benefit.

A variable annuity is designed to provide reliable monthly income that lasts for life. It is a long-term investment that can help you grow your retirement savings faster by investing in a diverse selection of investment options while deferring taxes until you take income. The market-based investment performance will be variable, meaning it can go up or down. Variable annuities also allow you to provide for loved ones through a guaranteed death benefit.

Being happily retired looks different for everybody. Maybe you want steady retirement income that lasts or supplemental income to help you meet the unexpected in life.

LEARN MORE

You don’t know what the future has planned for you, but you want to be prepared for the unexpected and be able to achieve your goals.

LEARN MORE

You want your business to maintain its competitive edge. Attracting talent and building a succession plan for the future means you can ensure your business stays in stable hands.

LEARN MOREBeing happily retired looks different for everybody. Maybe you want steady retirement income that lasts or supplemental income to help you meet the unexpected in life.

LEARN MOREYou don’t know what the future has planned for you, but you want to be prepared for the unexpected and be able to achieve your goals.

LEARN MOREYou want your business to maintain its competitive edge. Attracting talent and building a succession plan for the future means you can ensure your business stays in stable hands.

LEARN MOREThe primary purpose of a life insurance policy is to provide death benefit protection.

Life insurance is subject to underwriting and approval of the application, and will incur monthly policy charges.

In order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

Guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company and do not protect the value of the variable investment options, which are subject to market risk.

Pacific Life, its distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor or attorney.

Annuity withdrawals and other distributions of taxable amounts, including death benefit payouts, will be subject to ordinary income tax. For nonqualified contracts, an additional 3.8% federal tax may apply on net investment income. If withdrawals and other distributions are taken prior to age 59½, an additional 10% federal tax may apply. A withdrawal charge and a market value adjustment (MVA) also may apply. Withdrawals will reduce the contract value and the value of the death benefits, and also may reduce the value of any optional benefits.

Under current law, a nonqualified annuity that is owned by an individual is generally entitled to tax deferral. IRAs and qualified plans—such as 401(k)s and 403(b)s—are already tax‑deferred. Therefore, a deferred annuity should be used only to fund an IRA or qualified plan to benefit from the annuity’s features other than tax deferral. These include lifetime income and death benefit options.

For federal income tax purposes, tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death; (3) withdrawals taken during the first 15 policy years do not occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Secs. 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits.

For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2)(i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

All investing involves risk, including the possible loss of the principal amount invested. The value of the variable investment options will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please see the prospectus for a detailed description of investment risks.

The "S&P 500® index" is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by Pacific Life Insurance Company. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Pacific Life’s product is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500® index. The index is not available for direct investment, and index performance does not include the reinvestment of dividends.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life's Home Office is located in Newport Beach, CA.

PL1.2B